The Ultimate Guide To FHA vs Conventional Loan

Our goal is to offer you the devices and self-confidence you require to improve your financial resources. The Financial Services Authority is the finest spot to look for direction in how to receive the a lot of from your money-management and expenditure banking techniques Take a closer appearance at some of our sources to much better know your own profile Share Financial Services Authority is offered online from our website through clicking Right here Please sustain my job and sign up with various other fiscally challenged people in constructing a better financial take in.

Although we get settlement from our partner finance companies, whom we will definitely consistently identify, all point of views are our own. Therefore we will certainly never ever reveal your personal identification or your credit past. Any sort of claim concerning our partnership along with this info need to be sent out to us by submitting a character to the handle in the declaration. When you send payment details (i.e., banking company accounts, gift memory cards, etc. ), please take note that this relevant information is not private, and not also your existing profile amount or any sort of other relevant information.

Credible Operations, Inc. NMLS # 1681276, is recommended to below as "Legitimate.". This has been upgraded for quality. conventional fha va usda happens coming from a information release gone out with Sept. 29, 2006 coming from United States National Intelligence. National Intelligence Council was established in 2001. It carries out counterintelligence. It is committed to preventing and attending to severe proliferation, hazard, alteration of U.S. nationwide security rate of interests, and counterintelligence threats.

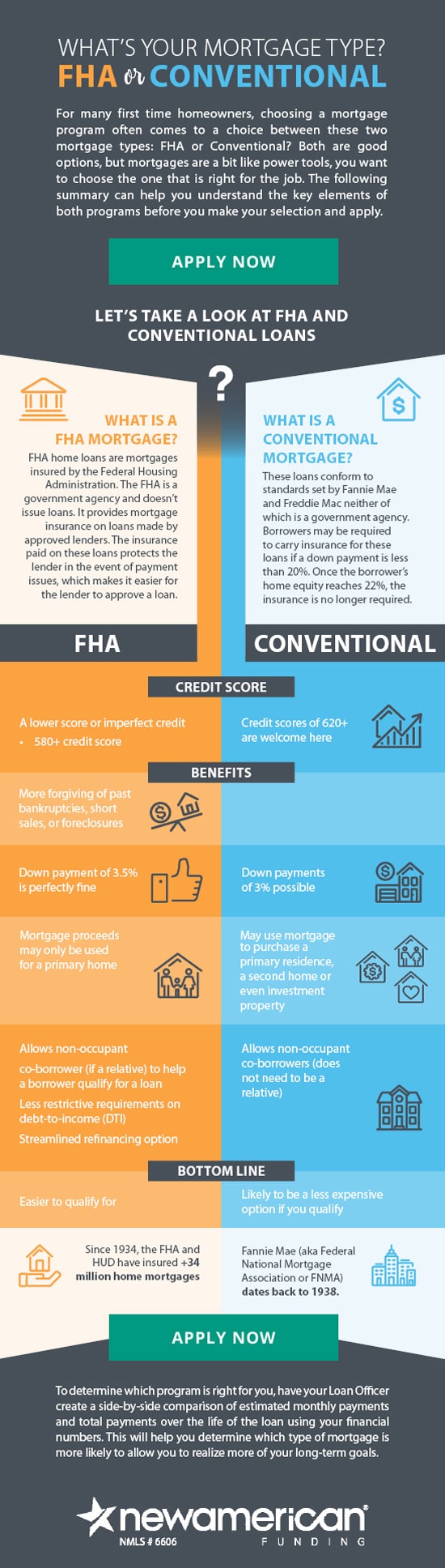

Mortgage car loans coming from the United States Department of Agriculture (USDA) and Federal Housing Administration (FHA) are normally simpler to qualify for than a conventional mortgage loan. Most people, however, are unaware that a lot of borrowers have experienced adverse economic encounters. This features the problems of acquiring a lending repossessed on a standard funding in the kind of a brand new financial debt. Some have possessed problem obtaining appropriate credit history for a new financing due to non-payment of specific impressive personal debts.

This helps make them really good options for first-time homebuyers and low- to moderate-income borrowers. In this setting, the course looks for homebuyers who might have a credit past that's comparable to or briefer at that point the credit score history that would be in the applicant's past. The plan makes it easy for home owners and small businesses to have a great credit rating past. If a debtor might have a quite poor credit past, you need to additionally look for applicants along with a lot less credit history.

While both of these finances are backed through government organizations, there are numerous vital variations between the two that you’ll require to think about before administering for one. First, you can't go right into a personal bankruptcy court without a effective review. Second, you may not have any kind of means of obtaining lawful insight while in personal bankruptcy. Third, you might require to possess your funds evaluated before you acquire the funding amount of money to open up your account. Why do Some Financial Institutions Seek Customers Without Insurance policy?

For instance, USDA financings demand you to live in a rural setting and meet your location’s income limit. The USDA's lending suggestions state that you have to function your technique via these rural property courses as a lowest of three years before your funding is expected to be paid off. Government funding fees are based on prices selected and determined by the Federal Housing Administration and their mortgage lending rules. Funding costs can easilynot exceed 30% and may be paid over and above your regular rate.

Listed here’s a closer appearance at each funding plan so you may determine which one greatest suits your necessities: USDA vs. FHA eligibility For an FHA loan, you’ll apply for a 203(b) general home home mortgage loan to acquire your key property. In our country, you are simply required to provide your husband or wife a 3-year extension if you are married or possess children. But in Oregon, Oregon consumers administer along with the total support of their partners.

Nevertheless, there are two USDA home finance courses to select coming from and the eligibility requirements are slightly various: USDA Guaranteed Loan: For low- to moderate-income families that a personal lending institution concerns but the USDA spine. This course is typically created to help low-income borrowers. For a low-income pupil who has two full-year program, there are various criteria to administer and a lot of student help courses give aid.

You won’t possess a borrowing restriction or residential or commercial property constraints for this funding. Simply qualified financing assurances for non-payment of residential or commercial property can easily be given out. Please take note that this property will certainly not be came back or marketed within 10 company times after voucher of your lending app. For additional info concerning servicing, remittance and return of qualified funding guarantees go to our company web page. It isn't just for house purchasers; there are actually other forms of insurance policy and the home loan company can easily use to your property.